by

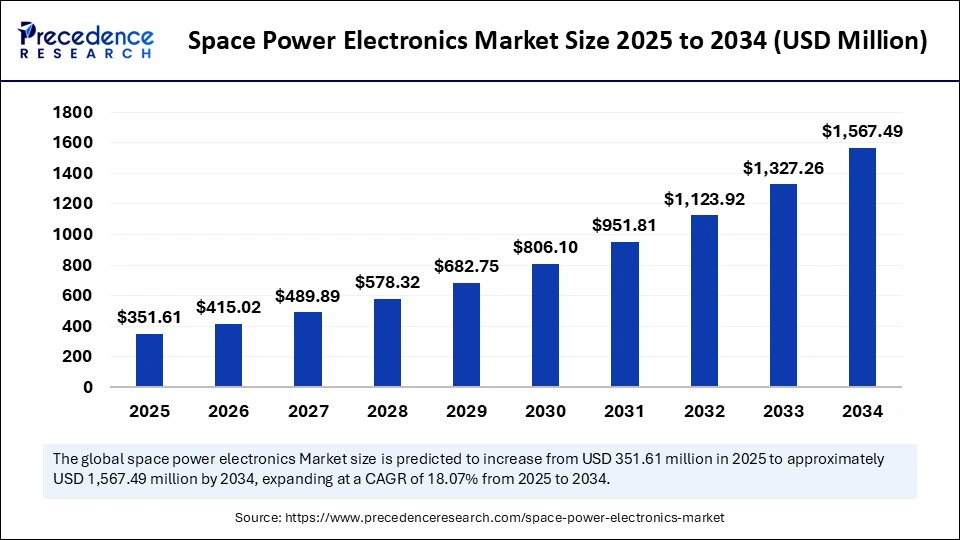

by The global space power electronics market, valued at USD 297.91 million in 2024, is projected to expand dramatically to approximately USD 1,567.49 million by 2034. This represents a robust compound annual growth rate (CAGR) of 18.07% between 2025 and 2034, driven by the surging demand for efficient, reliable power systems critical to satellites, spacecraft, and space exploration missions.

Key Market Insights

-

The space power electronics market stood at USD 297.91 million in 2024 and is forecasted to reach USD 1,567.49 million by 2034, growing at a CAGR of 18.07%.

-

North America dominated the market in 2024, holding a 37% share, with the U.S. market valued at USD 77.16 million.

-

Asia Pacific is the fastest-growing region, propelled by growing space programs in China, India, and Japan.

-

Key players include NASA, SpaceX, and major semiconductor innovators driving innovation in radiation-hardened components.

-

Power integrated circuits continue to dominate device types, while power modules are the fastest-growing segment.

-

Satellite power systems represent the largest application segment due to increased satellite deployments.

What Is Driving the Explosive Growth in Space Power Electronics?

The demand for miniature, reliable, and radiation-hardened power electronics is expanding with the increase in satellite launches and ambitious deep-space exploration projects. The market benefits from growing commercial space ventures, reusable launch vehicles, and heightened governmental investment in lunar and Mars missions. Advanced power electronics are essential for managing energy conversion, regulation, and distribution in the hostile conditions of space, where reliability can determine mission success or failure.

How Is AI Shaping the Future of Space Power Electronics?

Artificial intelligence is playing an increasingly pivotal role by enabling real-time optimization and autonomous fault detection in spacecraft power management. AI-driven algorithms predict maintenance needs and optimize energy distribution between payloads and propulsion systems, reducing risk and extending mission life. Moreover, machine learning assists in designing circuits hardened against cosmic radiation, accelerating innovation and enhancing spacecraft resilience, a critical factor for long-duration and deep-space missions.

What Are the Key Market Growth Factors?

-

The boom in satellite constellations for communications, Earth observation, and navigation is pushing demand for miniaturized and efficient power systems.

-

Rising defense and military programs necessitate highly reliable, secure power electronics for space-based reconnaissance and communications.

-

Advances in semiconductor materials like Silicon Carbide (SiC) and Gallium Nitride (GaN) are improving efficiency and reducing system weight.

-

The shift towards electric propulsion and deep-space missions is fueling the growth of high-voltage power electronics systems.

What Opportunities and Trends Are Shaping the Market?

Are small satellites changing the market dynamics?

The proliferation of CubeSats and nanosatellites is driving demand for cost-efficient, scalable power electronics that can be mass-produced and customized for diverse missions.

How is industry collaboration influencing innovation?

Collaborations among space agencies, private firms, and academic institutions are fostering rapid development of modular, adaptive power systems suitable for in-orbit servicing and manufacturing.

What impact does the rise of reusable launch vehicles have?

Reusable launch vehicles demand power electronics capable of enduring repeated thermal and mechanical stresses, motivating innovations in durability and fault tolerance.

What role do new materials play?

Emerging materials like SiC and GaN are expanding power density and efficiency benchmarks, crucial for next-generation propulsion and communication payloads.

How Are Regional Markets Shaped?

North America commands the largest share, driven by NASA, SpaceX, and a rich ecosystem of aerospace and semiconductor players that lead in technology development and deployment. The region’s robust investment environment and launch infrastructure secure its position as a global powerhouse.

Asia Pacific is rapidly emerging as the fastest-growing region, led by China, India, and Japan, driven by expansive national space programs and a rising wave of commercial satellite ventures. Governmental funding and cost-effective manufacturing bolster this growth.

Market Segmentation

By Device Type: Power integrated circuits dominate due to their compact size and multifunctionality, while power modules experience the fastest growth owing to higher power handling and modularity.

By Component: DC-DC converters hold a crucial role for voltage transformation, essential for satellite operations, with solid-state power controllers (SSPCs) as the fastest-growing for intelligent power distribution.

By Voltage Range: Medium voltage systems lead in application, balancing efficiency and safety, while high voltage systems are expanding rapidly to meet electric propulsion needs.

By Material: Silicon remains dominant, valued for cost-efficiency and reliability, but SiC and GaN are the fastest-growing materials, enabling higher performance.

By Application: Satellite power systems dominate, crucial for communication, navigation, and Earth observation, with deep-space missions growing fastest due to ambitious exploration efforts.

By End-User: Commercial space operators lead in market share, driven by private satellite constellations, with defense sectors expanding swiftly due to militarization of space.

Space Power Electronics Market Companies

- Airbus Defence and Space

- Thales Alenia Space

- Lockheed Martin Corporation

- Northrop Grumman Corporation

- BAE Systems plc

- Boeing Defense, Space & Security

- Raytheon Technologies Corporation

- Mitsubishi Electric Corporation

- STMicroelectronics

- Infineon Technologies AG

- Texas Instruments Incorporated

- Analog Devices, Inc.

- Microchip Technology Inc.

- Renesas Electronics Corporation

- Cobham Advanced Electronic Solutions

- Vicor Corporation

- VPT, Inc.

- GaN Systems Inc.

- Efficient Power Conversion (EPC) Corporation

- Power Integrations, Inc.

Challenges and Cost Pressures Facing the Industry

High costs for space-qualified, radiation-hardened electronics remain a major barrier. Prolonged testing, scarce raw materials, regulatory fragmentation, and supply chain limitations raise development expenses. Moreover, geopolitical tensions hamper technology sharing and complicate international collaboration.

Read Also: Aluminum Smelting Market

You can place an order or ask any questions. Please feel free to contact us at sales@precedenceresearch.com |+1 804 441 9344

- Managed DNS Services Market Size to Hit USD 2,288.60 Million by 2035 - March 5, 2026

- Power EPC Market Size to Hit USD 1,376.29 Billion by 2035 - March 5, 2026

- Ursolic Acid Market Size to Hit USD 68.77 Billion by 2035 - March 5, 2026