by

by Surging Diabetes Prevalence and Technological Breakthroughs Propel Market to 5.07% CAGR Through 2034

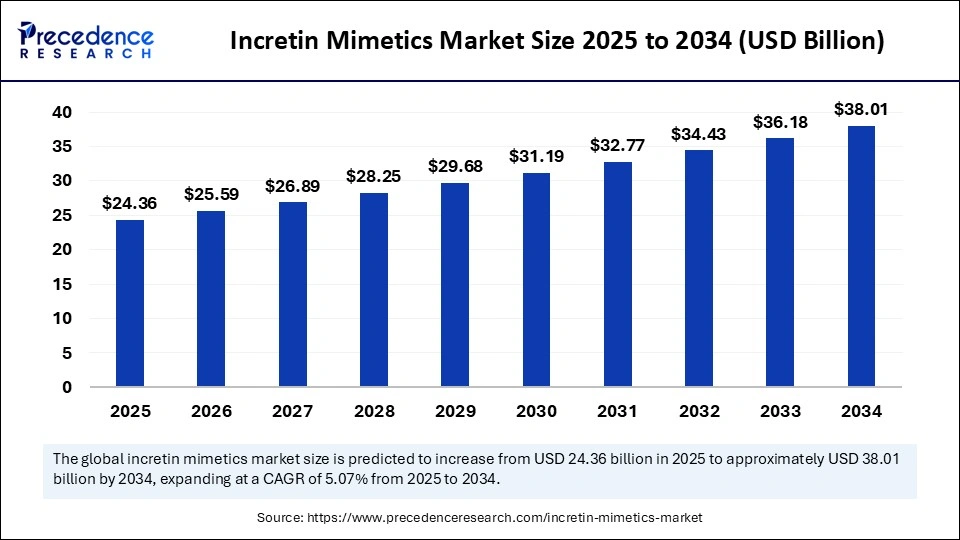

The global incretin mimetics market size is evaluated at USD 24.36 billion in 2025 and is predicted to increase from USD 25.59 billion in 2026 to approximately USD 38.01 billion by 2034, expanding at a CAGR of 5.07% from 2025 to 2034. With diabetes and obesity rates rising worldwide, advancements in GLP-1 analogs and AI-powered research are catalyzing the next leap in metabolic disease management. North America leads the market, while Asia Pacific stands out as the fastest-growing region powered by healthcare investments and expanded access.

Get this report to explore global market size, share, CAGR, and trends, featuring detailed segmental analysis and an insightful competitive landscape overview @ https://www.precedenceresearch.com/sample/7052

Introduction: Why Incretin Mimetics Matter

Driven by a convergence of diabetes prevalence, patient preference for convenience, and phenomenal R&D, incretin mimetics are redefining chronic disease care. These drugs, which closely imitate natural incretin hormones, offer not only precise glycemic control but also significant cardiovascular and weight management benefits—a combination reshaping therapeutic strategies globally.

Incretin Mimetics Market Key Insights

-

The global incretin mimetics market is valued at $24.36 billion in 2025 and forecast to reach $38.01 billion by 2034.

-

North America leads the market, with a 41.4% share and best-in-class healthcare infrastructure.

-

Asia Pacific is anticipated to grow fastest at a staggering 7.2% CAGR, fueled by increased diabetes diagnoses and healthcare spending.

-

GLP-1 receptor agonists dominate with more than 56% share, while dual/triple agonists are projected as the growth engine at 6.5% CAGR.

-

Subcutaneous injections remain the top delivery route, but oral formulations are gaining momentum with 7% annual growth.

-

Hospitals constitute just under 50% of the market’s end use, followed by clinics as the fastest-growing care setting.

-

Major companies include Novo Nordisk, Eli Lilly, AstraZeneca, Boehringer Ingelheim, and GSK, among others.

Incretin Mimetics Market Revenue Table

| Year | Global Market Size (USD Billion) |

|---|---|

| 2025 | 24.36 |

| 2026 | 25.59 |

| 2034 | 38.01 |

How AI Is Shaping the Incretin Mimetics Market

Artificial intelligence is becoming an indispensable force across the metabolic therapeutics landscape. AI-powered algorithms are now expediting the design and molecular simulation of novel incretin-based peptides, allowing for faster identification of drug candidates with optimal stability, efficacy, and side-effect profiles. Machine learning supports clinical trial patient selection, real-time monitoring, and predictive modeling, which in turn dramatically increases trial success rates.

On the manufacturing side, AI-driven analytics streamline peptide synthesis and purification—guaranteeing consistent product quality while minimizing operational waste. AI-enabled quality assurance platforms catch deviations immediately, boosting safety and regulatory compliance. With AI also helping to tailor therapies to patient subgroups, personalized diabetes and obesity care is shifting from concept to reality.

Incretin Mimetics Market Growth Factors: What’s Fueling Expansion?

Several powerful factors are driving the skyrocketing demand for incretin mimetics:

-

Rising global prevalence of type 2 diabetes and obesity, particularly among aging populations.

-

Unprecedented innovation in long-acting, combination, and oral peptide therapies improving patient adherence and outcomes.

-

Strategic collaborations between biotech startups and pharmaceutical giants pushing the frontiers of drug design and delivery.

-

Regulatory bodies expediting approvals thanks to robust efficacy and safety data.

-

Increased patient awareness around advanced therapies and the growing preference for highly convenient, once-weekly dosing.

Where Are the Opportunities and Trends?

What Makes Oral Formulations a Game Changer?

The surging demand for oral incretin mimetics is breaking barriers in metabolic care. Patients’ aversion to needles makes oral GLP-1 analogs and combination therapies incredibly attractive. Pharmaceutical innovators are leveraging advanced carrier systems and absorption enhancers, aligning with the broader trend toward non-invasive and patient-centric medication approaches.

How Is Sustainability Driving Market Strategy?

Companies are embedding green chemistry and recyclable injectors into product launches to meet global environmental mandates. Beyond reducing the carbon footprint in logistics, firms target ethically sourced peptides, waste minimization, and resource efficiency to appeal to an increasingly eco-conscious patient and investor base.

Which Tech Innovations Could Disrupt the Market Next?

Smart injectors with connected health monitoring, nanoscale peptide carriers, and bioprinting technologies are expected to redefine therapeutic delivery and efficacy. The convergence of digital health and pharmacology is creating new models for patient engagement and adherence.

Regional and Segmentation Insights

North America

North America dominates due to cutting-edge healthcare infrastructure, high diabetes incidence, and early access to next-gen treatments. Established reimbursement frameworks and major pharma players like Eli Lilly and Novo Nordisk are key to this region’s continued dominance. U.S.-based R&D, streamlined regulatory pathways, and widespread digital health adoption further strengthen the region’s leadership.

Asia Pacific

Asia Pacific’s market is surging with the fastest growth rate globally, influenced by rising incomes, chronic disease programs, and expanding clinical adoption. India is particularly notable for its biosimilar innovations and public-private research partnerships, while China and Japan contribute to increasing patient access.

Europe

Europe is posting sustained growth, aided by progressive reimbursement schemes, strong regulatory standards, and a determined push for sustainable manufacturing. Germany, with its pharmaceutical ecosystem and government incentives, leads continental innovation and collaboration.

Market Segmentation Table

| Segment | Market Share/Outlook |

|---|---|

| GLP-1 Receptor Agonists | 56.4% (Largest, 2024) |

| Dual/Triple Agonists | Fastest CAGR: 6.5% |

| Subcutaneous Injections | 70.4% (Dominant) |

| Oral Formulations | Fastest CAGR: 7.0% |

| Pre-filled Pens | 58.4% (Leading dosage form) |

| Hospitals | 48.5% (Largest end user) |

| Clinics | Fastest CAGR: 6.9% |

| Type 2 Diabetes | 54.4% (Top application) |

| Obesity/Weight Management | Fastest CAGR: 6.8% |

-

Novo Nordisk continues to lead with products like Ozempic and oral Rybelsus.

-

Eli Lilly’s Mounjaro has set benchmarks in dual agonist therapy.

-

AstraZeneca evolves its Bydureon and Byetta franchises.

-

Glenmark is ramping up affordable biosimilar access, especially in emerging markets.

-

Boehringer Ingelheim and GSK are intensifying R&D into long-acting, integrated therapeutics.

Incretin Mimetics Market Companies

-

Novo Nordisk A/S

-

Eli Lilly and Company

-

AstraZeneca PLC

-

GlaxoSmithKline PLC (GSK)

-

Boehringer Ingelheim GmbH

-

Glenmark Pharmaceuticals

-

Sanofi S.A.

-

Pfizer Inc.

-

Merck & Co., Inc.

-

Takeda Pharmaceutical Company Limited

-

Intarcia Therapeutics, Inc.

-

Zealand Pharma A/S

-

Hanmi Pharmaceutical Co., Ltd.

-

H. Lundbeck A/S

-

Lexicon Pharmaceuticals, Inc.

-

Viatris Inc.

Challenges and Cost Pressures: What Are the Barriers?

While innovation and demand soar, the market faces pressing challenges:

-

High R&D costs and complex manufacturing requirements for peptide-based drugs inflate overall treatment expenses.

-

Achieving scalable, cost-efficient production while preserving therapeutic integrity remains a persistent hurdle.

-

Regulatory scrutiny around safety and bioequivalence heightens the cost and time to market, especially for generics and biosimilars.

Case Study: Liraglutide and Semaglutide’s Real-World Impact

In October 2025, a landmark study of more than 21,000 military veterans showed that the GLP-1 agonists liraglutide (Victoza) and semaglutide (Ozempic) delivered comparable protection against kidney failure and major cardiovascular events, underscoring the class’s profound clinical value beyond glucose control.

Read Also: Type 2 Diabetes Management Market

You can place an order or ask any questions. Please feel free to contact us at sales@precedenceresearch.com |+1 804 441 9344

- Managed DNS Services Market Size to Hit USD 2,288.60 Million by 2035 - March 5, 2026

- Power EPC Market Size to Hit USD 1,376.29 Billion by 2035 - March 5, 2026

- Ursolic Acid Market Size to Hit USD 68.77 Billion by 2035 - March 5, 2026