by

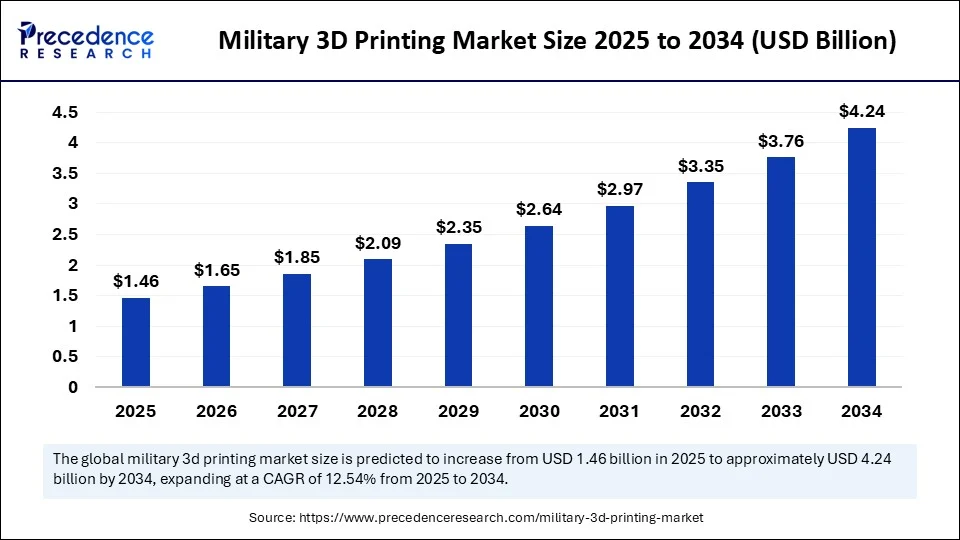

by The military 3D printing market is projected to grow from USD 1.30 billion in 2024, through USD 1.46 billion in 2025, and skyrocket to USD 4.24 billion by 2034, fueled by global defense upgrading initiatives, rising geopolitical tensions, and the increasing adoption of fast, decentralized manufacturing across military command structures.

Turbocharged Growth in Modern Defense

Accelerating at a CAGR of 12.54% between 2025 and 2034, the defense sector is leveraging 3D printing to manufacture mission-critical parts, prototypes, and customized equipment for battlefield and base environments. Key drivers include rapid prototyping, supply chain resilience, and new material innovations.

Military 3D Printing Market Quick Insights

- The military 3D printing market was valued at USD 1.30 billion in 2024 and is forecast to surpass USD 4.24 billion by 2034.

-

North America holds the largest market share, buoyed by advanced defense infrastructure and R&D investment, while Asia-Pacific is expected to be the fastest-growing region due to increasing defense budgets and tech adoption.

-

The U.S. market alone will expand from USD 327.60 million in 2024 to USD 1,091.06 million by 2034.

-

Fused Deposition Modeling (FDM) remains the most widely adopted technology, offering quick, cost-effective, and material-efficient manufacturing.

-

Metals & alloys dominate material segments for their strength, while ceramics & composites are on a rapid growth course for specialized uses.

-

The Army is the lead end user, and the Air Force is the fastest adopter due to high-performance aerospace component needs.

-

Direct procurement is the dominant distribution model, as militaries prefer tight control over confidential manufacturing processes.

Get this report to explore global market size, share, CAGR, and trends, featuring detailed segmental analysis and an insightful competitive landscape overview @ https://www.precedenceresearch.com/sample/6694

Military 3D Printing Market Revenue Table: Global and U.S. Market Breakdown

| Year | Global Market Value (USD Billion) | U.S. Market Value (USD Million) |

|---|---|---|

| 2024 | 1.30 | 327.60 |

| 2025 | 1.46 | 367.92 |

| 2034 | 4.24 | 1,091.06 |

Artificial Intelligence is revolutionizing military 3D printing by enabling smarter design, predictive maintenance, and manufacturing optimization. AI algorithms simulate battlefield conditions to refine, test, and strengthen prototypes before physical production, securing equipment durability and mission success. Additionally, machine learning models streamline supply chain planning and quality control, detecting flaws and reducing waste for reliable, high-speed delivery. This convergence supports autonomous manufacturing units, capable of functioning independently in conflict zones and remote setups.

Market Growth Factors: Powering the Shift

Defense modernization programs, rapid R&D, and demand for on-site, decentralized manufacturing are the backbone of market growth. Advanced polymer and metal printing technologies enable the production of vital equipment at the point of need, minimizing logistics, downtime, and operational vulnerability.

Are Military Logistics Ready for Transformation?

Can on-demand manufacturing reshape military logistics and enable real-time response in critical missions? The push is on to streamline supply chains and gain operational independence, with 3D printing offering a dramatic reduction in inventory and transport risks. Defense forces now fabricate spare parts and mission tools directly at bases—slashing turnaround time and boosting battlefield resilience.

Military 3D Printing Market Regional and Segmentation Analysis

Military 3D Printing Market Regional Landscape

-

North America: Dominates via advanced infrastructure, strong R&D, and robust supply ecosystems.

-

Asia-Pacific: Fastest-growing market, driven by rising budgets in China, India, South Korea, and Japan, and a drive towards defense self-sufficiency and technological innovation.

Segmentation Overview

By Technology

-

Fused Deposition Modeling (FDM): Cost-effective, rapid prototyping (largest share in 2024).

-

Direct Metal Laser Sintering/Selective Laser Melting (DML/SLM): Fastest growing for high-strength, complex metal parts—critical for aerospace and armored vehicles.

By Material

-

Metals & Alloys: Dominant material segment for structural and weapon components, valued for high stress and heat resilience.

-

Ceramics & Composites: Fast growth for protective armor and high-performance aerospace components due to lightweight and heat-resistant features.

By Application

-

Functional Parts Manufacture: Leading use case, enabling quick on-demand production to maintain operational continuity, reduce logistics, and customize supply chains.

-

Medical & Bioprinting: Fastest-growing segment, supporting on-site medical care, customized implants, and battlefield trauma management with advanced biomaterials.

By End User

-

Army: Largest consumer owing to vast component needs and tactical flexibility.

-

Air Force: Fastest growth fueled by lightweight, fuel-efficient aerospace applications and rapid prototyping demands.

By Distribution Model

-

Direct Procurement: Preferred for control and confidentiality, enabling responsive, secure part production.

-

Additive Manufacturing Service Providers: Fast-expanding; defense agencies access specialized expertise and advanced technologies without heavy in-house investment.

Which Innovations From Top Companies Are Shaping the Future?

Recent breakthroughs have come from leading defense, technology, and material firms, each expanding battlefield readiness and sustainability. Notable achievements involve:

-

High-strength, lightweight metal printing for unmanned aerial vehicles and armored vehicles

-

Mobile battlefield-ready printing units

-

Real-time medical bioprinting for trauma care and prosthetics

Military 3D Printing Market Companies

- 3D Systems Corporation

- Stratasys Ltd.

- EOS GmbH

- ExOne (Desktop Metal)

- GE Additive

- SLM Solutions Group AG

- Renishaw plc

- Materialise NV

- HP Inc.

Why Are Security, Cost, and Standards Still Roadblocks?

The sector faces persistent challenges around cybersecurity, quality standardization, and high deployment costs. Digital blueprint vulnerability, lack of uniform component standards, and skilled workforce requirements slow market expansion. Geopolitical restrictions and supply chain risks remain critical concerns, mandating greater investment in secure, certified additive manufacturing processes.

Case Study: Deploying Mobile 3D Printing Units in Combat Zones

For example, U.S. military field bases have successfully employed mobile 3D printing units to fabricate essential vehicle spares and medical tools, enhancing operational efficiency and lowering supply-chain dependency—even in high-risk environments.

Read Also: Underwater LiDAR Market

Want a Deeper Dive? Request Sample/Meeting

Discover how military 3D printing is redefining defense manufacturing standards. Download a free sample report or schedule a meeting with our market specialists at Precedence Research to explore the full report and customized advisory. Contact: sales@precedenceresearch.com

- Distributed Energy Resources Technology Market Size to Gain USD 293.59 Billion by 2034 - September 4, 2025

- Advanced Antenna Systems Market Size to Cross USD 21.00 Billion by 2034 - September 4, 2025

- Military 3D Printing Market Size to Surpass USD 4.24 Billion by 2034 - September 4, 2025