by

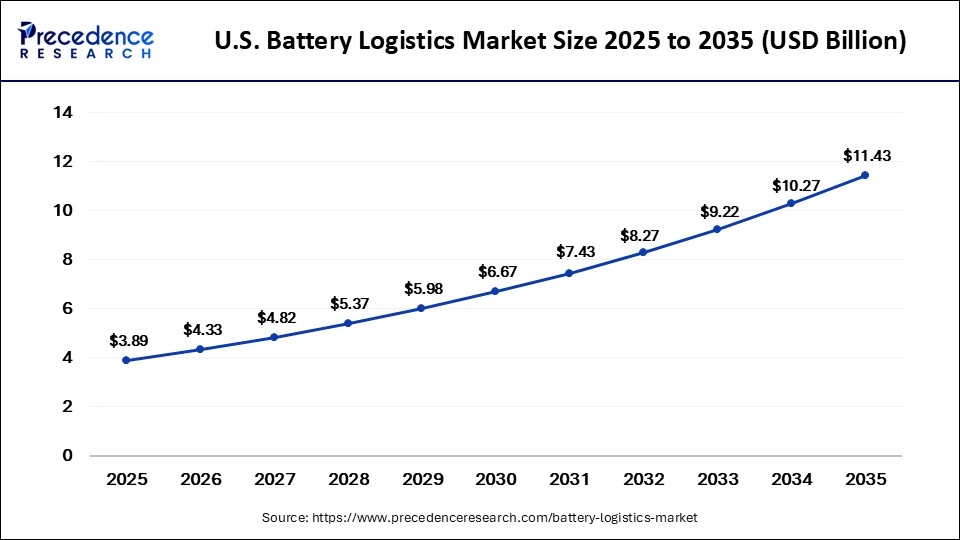

by The U.S. battery logistics market is projected to reach USD 11.43 billion by 2035, driven by EV production, battery manufacturing investments, and battery recycling initiatives.

Read Also: AI Hallucination Detection Market

U.S. Battery Logistics Market Overview

The U.S. battery logistics market is entering a phase of rapid expansion as electric vehicle (EV) adoption, battery manufacturing, and renewable energy storage deployments continue to reshape the nation’s industrial landscape. Efficient logistics solutions have become critical for safely transporting, storing, and managing batteries throughout their lifecycle.

According to industry estimates, the U.S. battery logistics market was valued at USD 3.89 billion in 2025 and is expected to grow from USD 4.33 billion in 2026 to approximately USD 11.43 billion by 2035, registering a CAGR of 11.38% during the forecast period.

Battery logistics includes transportation, warehousing, inventory management, packaging, distribution, reverse logistics, and recycling services. These operations support battery manufacturers, EV producers, energy storage providers, and electronics companies while ensuring compliance with strict safety regulations.

Key Highlights

- Market size reached USD 3.89 billion in 2025.

- Expected to surpass USD 11.43 billion by 2035.

- CAGR projected at 11.38% from 2026 to 2035.

- Lithium-ion batteries dominated the market in 2025.

- Transportation services accounted for the largest market share.

- Road transportation remained the preferred logistics mode.

- Electric vehicles represented the leading application segment.

- Automotive OEMs held the largest end-user share.

Rising EV Production Creating New Logistics Opportunities

The rapid growth of the electric vehicle industry remains the primary driver of the U.S. battery logistics market. Automakers are significantly increasing EV production capacity while investing heavily in domestic battery manufacturing facilities.

As battery gigafactories continue to emerge across the country, logistics providers are witnessing increasing demand for specialized transportation, warehousing, and inventory management solutions. The movement of battery materials, cells, modules, and finished battery packs requires dedicated infrastructure and compliance with hazardous materials regulations.

Industry analysts note that transportation is expected to remain the dominant battery logistics service due to the complex movement of batteries across manufacturing, assembly, and distribution networks.

Artificial Intelligence Reshaping Battery Supply Chains

Artificial intelligence is playing an increasingly important role in modern battery logistics operations. AI-powered systems help logistics providers improve route planning, monitor battery conditions during transit, optimize warehouse operations, and predict supply chain disruptions.

The integration of AI with IoT-enabled sensors and digital tracking platforms is enabling:

- Real-time shipment visibility

- Predictive maintenance

- Inventory optimization

- Enhanced safety compliance

- Reduced transportation costs

These technologies are improving operational efficiency while strengthening traceability throughout the battery supply chain.

Government Support Accelerating Market Growth

Federal initiatives aimed at strengthening domestic battery manufacturing and reducing supply chain dependencies are contributing significantly to market expansion.

Programs under the Inflation Reduction Act (IRA) and Infrastructure Investment and Jobs Act (IIJA) have encouraged investments in battery production facilities, critical mineral processing operations, and recycling infrastructure. These initiatives are increasing demand for transportation, storage, and distribution services throughout the battery ecosystem.

Market Drivers

Expansion of Domestic Battery Manufacturing

The construction of battery gigafactories and processing facilities across the United States is creating substantial demand for specialized logistics services. Manufacturers require reliable transportation networks capable of safely moving hazardous battery materials while maintaining operational efficiency.

Growing Energy Storage Deployments

Battery energy storage systems are increasingly being deployed to support renewable energy integration and grid modernization efforts. Rising energy storage installations are creating new opportunities for logistics providers specializing in battery transportation and storage.

Increasing Battery Recycling Activities

The growing emphasis on sustainability and circular economy practices is boosting demand for reverse logistics and battery recycling services. End-of-life battery collection and transportation are emerging as important growth segments within the industry.

Market Challenges

Stringent Safety Regulations

Lithium-ion batteries are classified as hazardous materials and require specialized handling, packaging, and transportation procedures. Compliance with federal and international regulations can increase operating costs and create logistical complexities.

High Infrastructure Investment Requirements

Battery logistics requires specialized storage facilities, trained personnel, advanced monitoring systems, and compliant transportation equipment, creating significant capital investment requirements.

Segment Analysis

By Battery Type

The lithium-ion battery segment dominated the market in 2025 due to widespread adoption across electric vehicles, consumer electronics, and energy storage systems.

Flow batteries are expected to register the fastest growth during the forecast period as utilities invest in long-duration energy storage projects.

By Logistics Service

Transportation services accounted for the largest market share in 2025 due to rising movement of battery materials and finished products across domestic and international supply chains.

Warehousing and storage services are anticipated to witness strong growth as companies invest in specialized battery storage infrastructure.

By Transportation Mode

Road transportation remained the dominant logistics mode because of its flexibility and ability to provide direct delivery services across manufacturing and distribution networks.

Multimodal transportation is expected to gain momentum as companies seek more efficient and cost-effective logistics solutions.

By Application

The electric vehicle segment held the largest market share in 2025, supported by rising EV production and favorable government policies.

Energy storage systems are expected to experience the fastest growth owing to increasing investments in renewable energy infrastructure and grid modernization projects.

By Battery Lifecycle

Finished battery distribution dominated the market due to increasing shipments from manufacturers to automakers and energy storage providers.

Recycling and second-life logistics are projected to expand rapidly as battery recycling initiatives gain momentum nationwide.

Regional Insights

California

California remains a leading market due to strong EV adoption, extensive battery manufacturing operations, and ambitious clean energy policies.

Texas

Texas is emerging as a major battery logistics hub supported by growing renewable energy capacity, battery manufacturing investments, and extensive transportation infrastructure.

Massachusetts

The state’s investments in energy storage technologies and battery research are creating new opportunities for logistics providers.

North Carolina

North Carolina is attracting significant battery manufacturing investments, contributing to growing demand for logistics and supply chain services.

Competitive Landscape

The U.S. battery logistics market is moderately consolidated, with major logistics providers investing heavily in battery-specific infrastructure and digital technologies.

Companies are focusing on:

- Expanding warehousing capacity

- Developing hazardous-material transportation solutions

- Enhancing reverse logistics networks

- Implementing real-time shipment monitoring

- Improving supply chain visibility

Leading Companies

- DHL Supply Chain

- FedEx Corporation

- UPS Supply Chain Solutions

- Kuehne+Nagel

- DB Schenker

- DSV A/S

- CEVA Logistics

- GEODIS

- Ryder System Inc.

- Expeditors International

- C.H. Robinson

- XPO Logistics

- J.B. Hunt Transport Services

- Nippon Express Holdings

- Lineage Logistics

Recent Industry Developments

Recent investments demonstrate the increasing importance of specialized battery logistics solutions. In June 2026, Maersk introduced a dedicated lithium-ion battery transportation solution across its North American ground freight network, supporting the growing EV and battery manufacturing ecosystem.

Additionally, ITS Logistics launched its Battery Logistics Hubs network to provide integrated warehousing and transportation solutions for lithium-ion battery and EV supply chains.

Future Outlook

The future of the U.S. battery logistics market remains highly promising. Rising EV adoption, increasing battery manufacturing investments, growing renewable energy deployments, and expanding recycling ecosystems are expected to drive sustained demand for specialized logistics services.

As battery supply chains become more sophisticated, logistics providers that invest in advanced technologies, compliance capabilities, and dedicated infrastructure will be best positioned to capitalize on emerging opportunities.

Get a Sample Copy: https://www.precedenceresearch.com/sample/8521

For inquiries regarding discounts, bulk purchases, or customization requests, please contact us at sales@precedenceresearch.com