by

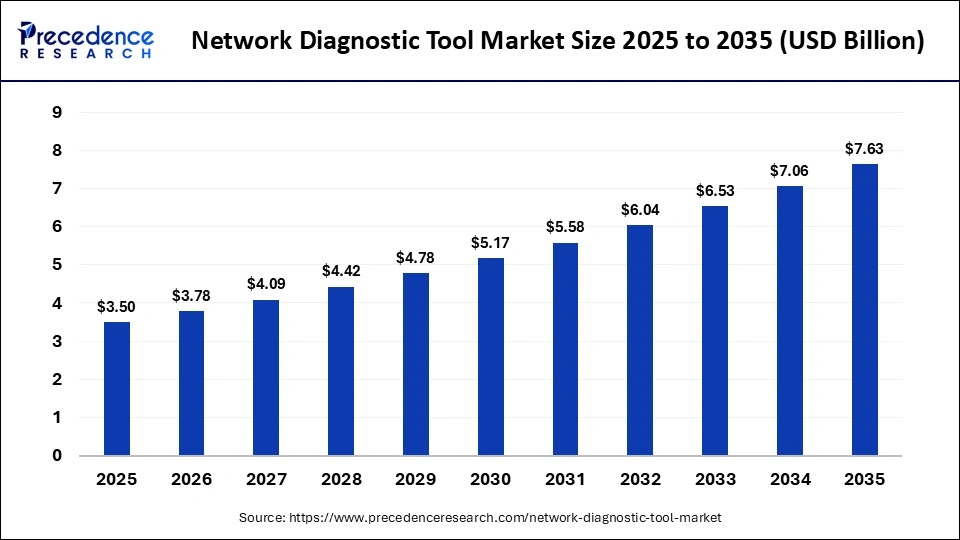

by The global network diagnostic tool market size was valued at USD 3.50 billion in 2025 and is projected to increase from USD 3.78 billion in 2026 to approximately USD 7.63 billion by 2035, expanding at a CAGR of 8.10% during the forecast period. The market is gaining strong momentum due to the increasing complexity of enterprise networks, rising use of hybrid cloud architectures, and growing need for real-time visibility into network performance. Enterprises across telecom, BFSI, healthcare, retail, and government sectors are increasingly investing in intelligent diagnostic tools to monitor latency, packet loss, traffic bottlenecks, and service disruptions before they affect business continuity.

As organizations adopt cloud-native applications, software-defined networks, remote work environments, and edge computing, maintaining network stability has become more difficult. Diagnostic tools are now being used to provide centralized observability, proactive fault detection, performance optimization, and security monitoring across distributed infrastructures. The rising convergence of networking and cybersecurity is also contributing to the market’s long-term growth outlook.

Read Also: AI Search Engine Market

Quick Insights

- The network diagnostic tool market was valued at USD 3.50 billion in 2025 and is projected to reach USD 7.63 billion by 2035.

- The market is expected to grow at a CAGR of 8.10% between 2026 and 2035.

- North America dominated the market with a 40% share in 2025.

- Asia Pacific is forecast to grow at the fastest CAGR of 10% through 2035.

- Cloud-based deployment held the largest share of 55% in 2025.

- The IT and telecommunication sector accounted for 40% of total market demand in 2025.

- Network performance monitoring tools led the market with a 35% share in 2025.

Network Diagnostic Tool Market Revenue Snapshot

| Metric | Value |

|---|---|

| Market Size in 2025 | USD 3.50 Billion |

| Market Size in 2026 | USD 3.78 Billion |

| Forecast Market Size in 2035 | USD 7.63 Billion |

| CAGR (2026-2035) | 8.10% |

| Largest Regional Market | North America |

| Fastest Growing Region | Asia Pacific |

How Is Artificial Intelligence Reshaping the Network Diagnostic Tool Market?

Artificial intelligence is rapidly changing the way organizations monitor and manage digital infrastructure. AI-powered network diagnostic tools can process large telemetry data streams from cloud, 5G, and edge computing environments much faster than traditional monitoring systems. These tools are increasingly being used to identify abnormal traffic behavior, detect latency spikes, predict outages, and automatically pinpoint the root causes of performance issues.

AI is also helping businesses improve network efficiency by reducing downtime and accelerating fault resolution. Companies are embedding machine learning algorithms into network observability platforms to automate troubleshooting, prioritize alerts, and provide predictive maintenance capabilities. The growing adoption of SD-WAN, SASE, and hybrid cloud infrastructure is expected to further strengthen demand for AI-enabled diagnostics. More than half of organizations now prefer AI-driven monitoring solutions because of their ability to improve uptime and optimize network performance.

What Are the Major Growth Drivers Supporting the Network Diagnostic Tool Market?

One of the strongest growth drivers is the rising adoption of cloud and hybrid IT environments. Businesses are increasingly moving mission-critical applications to multi-cloud ecosystems, creating more distributed and complex networks. Diagnostic tools help enterprises maintain visibility into latency, traffic flow, bandwidth usage, and service availability across these environments.

The rapid rollout of 5G networks and edge computing infrastructure is another key growth catalyst. 5G networks require sophisticated monitoring tools to support higher data throughput, network slicing, ultra-low latency, and a larger number of connected devices. At the same time, edge computing increases the need for localized diagnostics that can detect issues in real time. Global internet traffic rose by nearly 19% in 2025, increasing strain on telecom infrastructure and further accelerating demand for advanced network diagnostics.

The growing integration between network diagnostics and cybersecurity is also contributing to market growth. Businesses increasingly require tools capable of monitoring network health while simultaneously detecting abnormal traffic patterns, unauthorized access attempts, and suspicious activities across enterprise environments.

Why Are Cloud-Based Deployment Models Dominating the Market?

Cloud-based deployment dominated the market with a 55% share in 2025 because enterprises increasingly prefer scalable, flexible, and centrally managed monitoring environments. Cloud-based network diagnostic tools provide real-time visibility across distributed locations and remote work environments without requiring significant on-premises infrastructure investments.

The increasing adoption of edge-cloud integration, serverless computing, and hybrid work models is further boosting the demand for cloud-based diagnostic ecosystems. Businesses are leveraging these tools to improve network visibility, reduce operational costs, and accelerate deployment timelines. SaaS-based monitoring solutions are also becoming more attractive because of their lower upfront costs, automatic updates, and easier integration with cloud-native applications.

What Opportunities Are Emerging from 5G and Edge Computing?

The deployment of 5G and edge computing infrastructure is expected to create some of the largest long-term opportunities for the network diagnostic tool market. Telecom operators require advanced monitoring platforms to manage network slicing, virtualized network functions, and increasing traffic volumes associated with 5G environments. More than 1.2 billion global 5G connections were recorded in 2024, creating a major need for advanced testing, monitoring, and service assurance tools.

Edge computing is also creating new demand because it moves data processing closer to users and connected devices. Organizations deploying industrial IoT, smart manufacturing, autonomous systems, and connected healthcare technologies require localized monitoring solutions capable of delivering real-time visibility and low-latency diagnostics. By 2026, global edge IT infrastructure and data center spending is expected to exceed USD 314 billion, further boosting the need for advanced network diagnostics.

Which Product Segments Are Leading the Market?

Network performance monitoring tools led the market with a 35% share in 2025 because enterprises require continuous monitoring of bandwidth, latency, speed, and overall network performance. These tools are becoming essential for maintaining service quality across enterprise, telecom, and cloud-based environments.

Network traffic analyzer tools held the second-largest share of 30% in 2025 and are expected to grow at a CAGR of 8.5% during the forecast period. These tools are increasingly used to analyze traffic patterns, identify bottlenecks, improve bandwidth allocation, and strengthen security visibility. Meanwhile, network configuration and change management tools are expected to record the fastest growth because of the rising need for compliance, automation, and risk reduction across enterprise networks.

Why Does the IT and Telecommunication Sector Lead the Market?

The IT and telecommunication sector dominated the market with a 40% share in 2025 because telecom providers operate highly complex networks that require constant monitoring and optimization. These organizations depend on advanced diagnostic solutions to maintain uninterrupted voice, data, video streaming, and cloud services. Global 5G connections surpassed 2 billion in 2025, intensifying the need for reliable network performance monitoring across telecom infrastructure.

The BFSI segment held the second-largest share of 25% in 2025 because financial institutions require secure, reliable, and continuously monitored networks to support sensitive transactions and digital services. Government and healthcare organizations are also emerging as major users of network diagnostic tools because they increasingly rely on digital infrastructure, cloud services, and connected systems.

Why Is North America Dominating the Global Market?

North America accounted for 40% of the global network diagnostic tool market in 2025 due to the region’s advanced digital infrastructure, strong cloud adoption, and high concentration of hyperscale data centers. The region has seen rapid adoption of 5G, edge computing, and software-defined networking, increasing the need for real-time monitoring and observability solutions. North America recorded more than 314 million 5G connections in 2025, highlighting the strong need for advanced diagnostic tools.

The United States remains the dominant country-level market because of its large enterprise IT ecosystem, advanced telecom infrastructure, and rapid adoption of AI-powered monitoring platforms. Europe remains the second-largest regional market, supported by strong cybersecurity regulations and growing digital infrastructure investments. Asia Pacific is expected to witness the fastest growth because of expanding mobile connectivity, increasing cloud adoption, and large-scale telecom infrastructure investments across China, India, Japan, and South Korea.

What Challenges Could Limit Market Growth?

Despite strong growth prospects, the network diagnostic tool market faces several challenges. High implementation costs remain one of the biggest barriers, especially for small and medium-sized enterprises with limited IT budgets. Advanced diagnostic platforms often require substantial investment in software, hardware, integration services, and employee training. Nearly 39% of smaller organizations cite integration costs as a major obstacle to adoption.

Integration complexity is another major concern because many enterprises continue to rely on legacy systems that are difficult to connect with modern observability platforms. Additionally, there is an ongoing shortage of skilled professionals capable of managing AI-powered diagnostics, cloud-based monitoring tools, and advanced network analytics systems.

Case Study: Automated Fault Management Reduces Resolution Times

Telecom operators are increasingly adopting automated fault management systems to improve service continuity and reduce downtime. According to TM Forum, automated fault management reduced incident resolution times by more than 40% across large telecom networks in 2025. This demonstrates the growing value of AI-powered network diagnostics in helping businesses maintain uptime and improve customer experience across increasingly complex digital infrastructures.

Get Sample Link: https://www.precedenceresearch.com/sample/8313

For inquiries regarding discounts, bulk purchases, or customization requests, please contact us at sales@precedenceresearch.com

- Digital Infrastructure Market to Reach USD 1.32 Trillion by 2035 - June 10, 2026

- Ethoxyquin Market Size to Reach USD 446 Million by 2035 - June 10, 2026

- Liquid Crystal Polymer Market Poised to Reach USD 3.82 Billion by 2035 - June 3, 2026